Car finance compensation: 2026 Rules, Averages, and Claim Caps

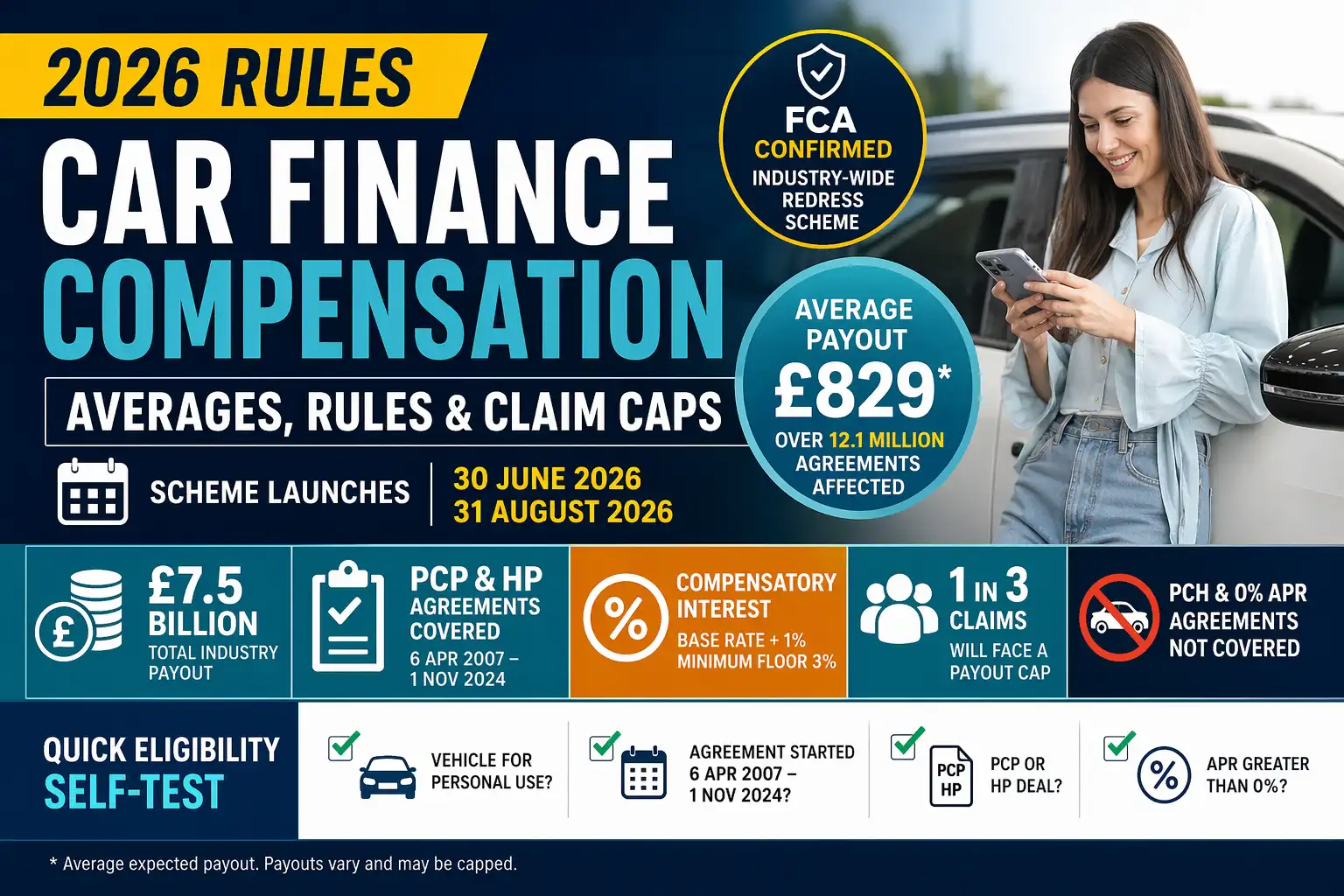

The Financial Conduct Authority confirmed an industry-wide redress scheme on 30 March 2026. This changes everything for millions of UK drivers. Over 12.1 million agreements are affected. The total industry payout should hit £7.5 billion, making this the biggest UK consumer finance event since PPI.

The headline average payout sits at £829. But there is a catch. Strictly defined eligibility criteria and hidden compensation caps mean you must understand the rules before submitting a claim.

The FCA’s car finance compensation scheme allows UK consumers to claim back excess interest charged through hidden discretionary commission arrangements on PCP and HP agreements taken out between 6 April 2007 and 1 November 2024. The average expected payout is £829, launching officially in mid-to-late 2026.

Key Takeaways

- The official scheme launches in two phases: 30 June 2026 and 31 August 2026.

- Eligible agreements span from 6 April 2007 to 1 November 2024.

- Personal Contract Purchase (PCP) and Hire Purchase (HP) are covered. Personal Contract Hire (PCH) is not.

- Payouts average £829, but roughly one in three claims will face a compensation cap.

- Lenders must calculate compensatory interest at the Bank of England base rate plus 1%. This comes with a strict 3% minimum floor.

Quick Start: The 60-Second Eligibility Self-Test

Answer YES to the following questions to see if you pass the initial gateway. If you answer NO to any of them, you are not eligible under the current scheme rules.

- Vehicle Type: Was the vehicle (car, van, or motorbike) for personal use?

- Date Range: Did the finance agreement start between 6 April 2007 and 1 November 2024?

- Finance Type: Was it a Hire Purchase (HP) or Personal Contract Purchase (PCP)?

- Interest Rate: Was your APR greater than 0%?

If you answered YES to all four, you pass the initial test. You should formally request your lender to check your file for a discretionary commission arrangement (DCA), an undisclosed tie, or an unfairly high commission setup.

Pro Tip: Rule out leases immediately. If your paperwork says “Personal Contract Hire” (PCH), do not waste time applying. The scheme only covers PCP and HP.

What is the 2026 FCA Motor Finance Redress Scheme?

The regulator stepped in to replace individual complaints with a mandated, industry-wide system. This stops lenders from ignoring you. It guarantees a set legal process for refunds.

However, you must stay alert to bad advice. Alison Walters, FCA Director (2026), warns: “Consumers should be wary of adverts that overpromise or give the impression they are endorsed by the FCA.” You can verify the exact wording via the FCA official announcement.

The Dates You Need to Know

Your finance start date dictates your claim timeline. The scheme covers contracts spanning a massive 17-year window. It includes agreements signed between 6 April 2007 and 1 November 2024.

The actual payout scheme launches on two different dates.

Pro Tip: Check your date bracket first. If your loan started between 1 April 2014 and 1 November 2024, your scheme date is 30 June 2026. If your loan is older (starting between 2007 and March 2014), you must wait for the 31 August 2026 launch.

Exclusions: The £150 Rule and 0% APR

Not every bad deal qualifies for a refund. The FCA excluded certain agreements to focus on severe consumer harm.

Agreements with 0% APR are completely excluded. The FCA also confirmed that deals involving minimal broker commission do not qualify. Specifically, if the commission was £120 or less before April 2014, or £150 or less after that date, the agreement is entirely excluded from the redress scheme.

Common Mistake: Thinking a high monthly payment automatically means you were mis-sold. Your eligibility relies entirely on the hidden commission paid to the broker, not just a high interest rate.

How Much Could You Get? (£829 Average vs. Capped Claims)

Many drivers fixate on the £829 average payout. That number comes from dividing the massive £7.5 billion industry pot among expected claimants. But that average hides a hard truth.

The FCA will cap payouts for roughly one in three people. This rule prevents “unjust enrichment”. The regulator refuses to put consumers in a better position than they would be in a genuinely fair market.

Mini Case Study: A driver financed a van via Hire Purchase in 2011. The broker received an unfairly high commission. However, the overall interest rate remained somewhat competitive for the market at that time. The driver falls into the one-in-three category facing a payout cap. They still secure a refund of the unfair markup with a 21% estimated loss factored in, but they receive slightly less than the headline £829 average.

Pro Tip: Expect a cap if you suffered no real financial loss compared to standard market rates at the time.

The 39% “High Commission” Threshold

Brokers often took a huge cut of the loan cost. To streamline claims, the FCA defined exactly what “high commission” means. An arrangement is classed as high commission if the broker’s cut accounted for at least 39% of the total cost of credit, and at least 10% of the total loan amount.

| Finance Type | Eligible for Redress? | Compensatory Interest Included? | Common Usage |

| Personal Contract Purchase (PCP) | Yes | Yes (Base + 1%, min 3%) | Standard personal car finance |

| Hire Purchase (HP) | Yes | Yes (Base + 1%, min 3%) | Vans, motorbikes, outright ownership |

| Personal Contract Hire (PCH) | No | No | Car leasing and rentals |

Mid-Point Recap

- You need a PCP or HP deal signed between 2007 and 2024.

- Your broker or dealer must have used a DCA or High Commission model.

- Payouts include an 8% compensatory interest rate floor, calculated at Base Rate plus 1%.

- Low commission deals under £150 are entirely disqualified.

Step-by-Step: How to Claim Your Car Finance Refund

Getting your money back requires action. Do not just wait around. You need a clear strategy to force your lender’s hand.

Claim Readiness Checklist

- [ ] Identify the Lender: Your claim goes to the finance provider, like Black Horse or MotoNovo. Do not complain to the car dealership where you bought the vehicle.

- [ ] Gather the Agreement Number: Find your original contract. You can also check old bank statements for the direct debit reference used for your monthly payments.

- [ ] Verify Address History: Have you moved since taking out the loan? Gather your previous addresses to pass security checks with the lender.

- [ ] Check the Scheme Date: Mark your calendar for 30 June 2026 or 31 August 2026. This ensures your lender meets their mandatory response deadlines.

Here is the exact process you should follow to start your claim:

- Identify your actual finance lender.

- Locate your specific agreement number.

- Submit a formal query asking if a discretionary commission arrangement was attached to your loan.

- Await the mandatory three-month lender response.

Pro Tip: Do not pay claims management fees. You do not need a paid firm to get your money. You can submit complaints to your lender directly for free. Free guidance is available via the MoneyHelper claim guide.

Common Pitfalls and the “Proactive vs. Reactive” Trap

Many drivers plan to sit back and wait for a cheque in the post. This is a massive mistake.

The FCA rules state lenders are legally required to contact people who have not complained. They must do this within six months of the relevant implementation period ending if they are likely owed money. But waiting puts you entirely at the back of the queue.

Pro Tip: Do not wait for lenders to find you. Submitting your complaint right now triggers a faster timeline. It legally binds the lender to a strict three-month response window. Take control of your claim immediately.

Beware of Social Media Scams

Fraudsters know millions of people are owed money. They are flooding social platforms with fake adverts to steal your details.

Pro Tip: Ignore social media ads using unauthorised AI videos of celebrities promising thousands in car finance compensation. Rely strictly on official FCA or direct lender correspondence.

What if the Lender Rejects Your Claim?

Not every lender will agree with your assessment. Sometimes they reject valid complaints or offer a payout you think is too low. Do not panic.

You can escalate disputed claims to the Financial Ombudsman Service. This is an official, independent UK body. It exists to resolve disputes between consumers and financial firms. You can read their specific guidance on the Financial Ombudsman vehicle finance portal.

Typical scenario example: A consumer took out a PCP agreement for a family car in 2016. The dealer used a DCA to bump the interest rate, increasing their own payout. Under the FCA’s Scheme 2 rules, the consumer complained proactively. The lender was forced to confirm the compensation amount within three months. They offered a full refund of the excess commission paid. They also added 17% of the interest paid as an estimated loss, topped with the minimum 3% compensatory interest.

The regulator expects firms to handle complaints efficiently. As the FCA stated in 2026: “An industry-wide scheme is the quickest and most cost effective way to deliver fair compensation.”

End Summary

The 2026 scheme provides a structured, legal pathway to reclaim hidden commission on PCP and HP agreements. However, strict rules dictate the final outcome. Understanding the £150 minimal commission threshold and the payout calculation caps ensures you are not caught off guard. You must take proactive steps to secure your refund.

Next Steps:

- Find your original finance agreement paperwork or bank statement references today.

- Determine if your loan falls into the Scheme 1 or Scheme 2 launch dates.

- Submit a direct, free inquiry to your lender immediately to trigger the three-month response timer.

FAQs

Can I claim car finance compensation if I have already paid off the car?

Yes. You can claim on settled agreements as long as the contract started between 6 April 2007 and 1 November 2024.

Does the FCA scheme cover van and motorbike finance?

Yes. Hire Purchase and PCP agreements for vans and motorbikes are fully covered, provided the vehicle was primarily for personal use.

How long does a car finance claim take in 2026?

If you complain proactively, lenders are legally bound to a three-month response window once the scheme officially launches for your specific date bracket.

Do I need a Claims Management Company to get my car finance refund?

No. You do not need to pay a third party. You can complain directly to your lender for free under the official FCA scheme.

What happens if my car dealership has gone bust?

Your claim is against the finance provider that lent you the money, not the dealership that sold you the car. The dealership’s status does not affect your claim.

Can I claim if my car finance was 0% APR?

No. The FCA confirmed that all 0% APR agreements are completely excluded from the redress scheme.

How is the interest calculated on my car finance payout?

Lenders must pay simple interest on your compensation. This is calculated at the annual average Bank of England base rate plus 1%, with a guaranteed minimum interest rate floor of 3%.